For my latest musings - please visit www.scottreeve.com

===================

This is my take on the world economy - Preserve your wealth while you still can!

The current talk is that the US and Europe may go back into recession. The reality is that they never left recession that hit in 2008. Bogus diluted statistics, such as inflation, unemployment rates have falsely portrayed the economic reality being felt by individuals in towns and cities around the world. Arguably many cities have been in depression for the last decade (look at Detroit and parts of Europe). The world economy is now on a detox diet and it will take many years, if not decades, to clean it up.

The markets are currently discounting that something very, very big is soon to happen. The markets always do this long before the average man on the street and the media realise it.

It could be a combination of things:

*country default;

* Euro monetary changes (Greece is insolvent, and other countries are close behind);

* central bank quantitative easing (monetising debt);

* major bank failure (particularly in Europe); and

* a significant slowdown in China.

All of these things are very real and we are already seeing the effects of this on world markets.

European contagion

All the major Euro countries are so intertwined lending billions to each other. A contagion will quickly spread when more of the bad debts rise to the surface.

Most of the current Euro-cris discussion is centred around Greece. By many measures its economy looks quite sick. It's sharemarket is now at its lowest level in 18 years (This is debt implosion!).

On other measures it certainly doesn't look as bad as other countries. Greece doesn't have the largest amount of government or private debts in the world, or the highest debt-to-GDP. One big difference is that it owes a much higher per cent of its debt to foreign creditors (foreign banks and countries).

Many argue that its non-sovereign entities which are clamping down on Greece. ie. the Global banking cartel led by the IMF, the World Bank, the Federal Reserve etc working in tune with the credit rating agencies (Moodys, S&P, Fitch). All I ask is what is the interests of the global banking groups? All actions to date show that they put their interests and survival ahead of everyone else. They do not care about the sovereignty of nation states.

So which countries banks' have the most at stake with Greece?

The following interactive chart I put together uses Bank for International Settlements data demonstrating which countries banks are most exposed to sovereign Greek debt as of the first quarter ending March 31 2011.

The most exposured banks are (by country):

French banks US$56.9 bn;

German banks US$23.8 bn;

UK banks US$14.7 bn;

The most exposed individual banks are:

BNP Paribas with US$7.1 bn (France)

Dexia with US$4.8 (Belgium)

Société Généralewith US$3.8 (France)

This is just the banks. When you add Government's holding Greek debt the amount is another US$145 bn.

Chart : There has been a huge widening of bony yield spreads and risk insurance on credit default swaps. Greece has gone parabolic. Portugal and Ireland are where Greece was a year ago.

or as Alan Kohler puts it, when the financial crisis hit last time in 2008, it was about liquidity (banks wouldn't lend to one another). This time around its about insolvency. There is plenty of cash around, but the banks might be broke.

Chart:

source: Alan Kohler, ABC News, Sept 2011

source: Alan Kohler, ABC News, Sept 2011The dominoes are lined up

The next graph shows why the banking system is trying to fix Greece before it sets a precedent. You may have heard that Spain and Italy are "too big to fail, too big to bail". Europe bank exposure to Spain and Italy's are 6 to 7 times worse than Greece.

Chart :

The harsh reality is that no industry should be bailed out, including the banks from country to country. The ongoing debt crisis has come about because banks have lended and taken billion dollar bets to keep this unsound monetary system going (which is based on nothing but paper money generated out of nothing).

Monetary systems do blow up - why is the Euro any different?

One article I came across discuses that country default is more common than we are led to believe. There were a number of large defaults in the 1980s and 1990s in emerging countries across the Americas and eastern Europe. Economist Carmen Reinhart states that the list of deadbeat countries included

"current investor favorites like Brazil, which defaulted in 1983, went through a bout of hyperinflation in 1990 and effectively defaulted again, for the same reason, in 2000"

Reinhart and Professor Rogoff show that, on average, nations add 86% to their debt loads within three years of a credit crisis. At the same time, government revenue falls an average of 2% in the second year after the onset of the troubles. The way things are heading Greece and other Euro countries are heading down this path. Debts need to be rolled over...just like...a few snow flakes can lead to an avalanche.

The Stumble Cycle

Sovereign defaults--when a country stops paying its bills--go in waves, often following global financial crises, wars or the boom-bust cycles of commodities. Some countries, like Spain and Austria, mend their ways; others, like Argentina, are repeat offenders.

Chart :

The combination can be fatal for investors holding bonds issued by financially shaky countries like Argentina or Greece, which sell a lot of their debt outside their own borders (as does the U.S.--45% of all publicly held debt). As a nation's finances deteriorate, foreign investors sell their bonds, putting upward pressure on interest rates. That usually sets off a spiral including a deteriorating currency, which, if the bonds are denominated in foreign currencies, makes it impossible for the country to pay its debt. Greece doesn't have to worry about this last syndrome, because it uses the euro. But that might make things worse since it can't print its way out of its financial difficulties. "It's like entering a prize fight with one hand tied behind your back," Bass says. Argentina takes a different tack. Still struggling in the wake of its 2002 default on foreign-held debt, its president recently tried, and failed, to seize central-bank dollar deposits (and cashier her central banker) in order to repay overseas debt.

France

Following from earlier discussion, the big questions are which of the big European banks will go under first. The largest French banks, Credit Agricole and Societe Generale have billions in exposure to Greece and other Euro countries.

Chart : The share prices of the 3 largest French banks have fallen 73%, 87% and 87% since start the debt crisis started in 2008.

Italy

Until recently UniCredit was the largest bank in Italy by market capitalisation and a major euro-zone bank. It owns other large banks in Germany, Austria, and Poland with around 40 million customers all up. As the following charts shows, the market is dumping the two largest Italian banks. UniCredit is one of the "too big to fail and bail" euro banks and many of its depositors lie outside Italy, making and bail out practically impossible.

An ironic twist to this is that, UniCredit's predecessor was a bank called

Credit-Anstalt. This bank collapsed in 1931 which lead to a contagion which took Europe off the gold standard and pro-longed the Great Depression. Few people remain from the last depression era. Perhaps the money lessons need to be relearn?

Chart :

Australian dollar

The Australian dollar is a proxy for commodity prices and ultimately China. The Australian dollar has recently fallen sharply to 97 cents and has hit a major support level. If this fails there is another major support level at 94 cents.

Chart: The Australian dollar managed to bounce off the firs support level at US$0.97

Commodities

Overall commodity prices are not showing that China is in immediate trouble. Base metals: copper, zinc, nickel, lead etc are not in a major bear market yet. This may mean that the current correction will be short lived. If base metals start free falling and other negative signs come from China (popping of housing bubble?), than the Australian dollar and commodity prices will fall a lot (a huge amount) further.

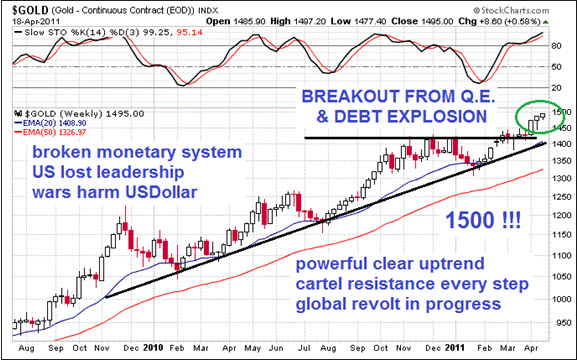

Gold

Meanwhile, gold and silver have recently experienced a significant correction. Chart wise (USD/gold), gold's correction is not unhealthy. Gold was sitting at 11 year bull-market resistance line and its trending support line is about US$1550.

Chart:

As I posted recently, I believe the gold demand is getting stronger, and will remain strong, despite the recent price volatility. Since that post it has been reported that Mexico, Russia, South Korea and Thailand have all made large purchases in 2011 and globally, central banks are set to buy more gold this year than at any time since the collapse of the Bretton Woods system 40 years ago. The IMF even reported that European Central banks have started accumulating small quantities of gold after selling on average 400 tonnes of gold a year since 1999.

Silver

Silver plummeted last week by 34 per cent within trading days. It went straight through two key support levels and bounced back above them. After hitting a low of US$26.03, silver rebounded 28 per cent in 28 hours.

Chart: Silver fell 34 percent within 4 trading days, then bounced 28 percent within 28 hours

Is this volatility unusual? Silver is a very small market and historically has been prone to major corrections. My research shows that the major corrections in the last few years has lead to an increase in demand for physical silver (from mints and bullion dealers). I believe this will happen again.

Australia

Take away mining and Australia is in recession, and as I stated early, the key to the Australian economy is whether China can keep its economy upright. If it shows signs of weakness, commodity prices will collapse (along with oil, gold and silver) and the Australian Dollar will fall 10 or 20 cents against the USD.

China kept the world economy somewhat afloat during the global financial crisis, and is the sole reason why Australia didn't go and stay into a technical recession. One of the key barometers on the health of China is commodity prices.

Tourism has been in recession for many years now, in part to the high Australian dollar and a tightening of consumer belts.

Manufacturing has largely been in recession for a number of years except for businesses with astute management and niche business models.

Manufacturing insolvencies growing

Despite insolvencies around the world dropping to their lowest levels in nearly four years, Australia is headed in the opposite direction. This year is shaping up to be a record one for business failures on a par with troubled Eurozone countries. The most recent D&B Global Insolvency Index, ranking business failures in more than 30 key economies, found Australia's insolvency rate was on a par with indebted countries such as Italy, Spain and Hungary. Australia recorded a 12.1 per cent increase in business failures in the June quarter compared with falls elsewhere in the world of 5.7 per cent. D&B said its findings tied in with Australian Securities and Investments Commission data which pegged 2011 as a record year for insolvencies.

Business failures in manufacturing have soared 60 per cent in three years. Almost 300 manufacturing firms went broke in the first six months of this year, the business analyst Dun & Bradstreet says, and just 14 new manufacturers started up. By contrast, in 2008, 974 new manufacturers got off the ground, and only 392 folded.

Retail

Retail is finally entering recession. This has long been coming, even though the likes of Westfield (and other groups) have been creating mega-shopping centres around Australia. The whole retail industry relies on ever increasing amounts of debt (more credit cards and increasing consumption). This model is dead, and there is currently too much competition in Australia alone (before you look at internet shopping of overseas products on eBay and the like). Take electronics, there are so many major stores competing on price, and margins are getting thinner. Many of the private equity firms which bought up a lot of the retailers in recent years have failed, as over-inflated sales targets have missed the mark. In the last 12 months several major groups have entered administration: REDGroup (Borders/Angus and Robertson bookstores); Colorado Group (Jag, and shoe shops), Allied Brands (Baskin Robbins, Cookie Man), Krispy Kreme doughnuts, and Starbucks Australia. Most recently sharper falls in consumer spending has forced Harvey Normany to scrap its Clive Peeters and Rick Hart brands (7 stores to close) and David Jones announcing a 10.3% drop in fourth quarter sales and now expects a small profit for the new financial year.

Sizeable retrenchments are coming.

Housing

Chart:

Lastly, this is a very good presentation by Mike Maloney

Cheers

~ Scott

{kind=link}